|

| Tuesday, 7 August 2018, 10:00 HKT/SGT | |

| |  | |

Source: SingSaver | |

|

|

|

SINGAPORE, Aug 7, 2018 - (Media OutReach) - Singaporeans are big credit card fans - and an improving economy means consumers are swiping plastic more frequently than ever. But beneath this exuberance lurks the risk of escalating debt, which can have dire consequences for individuals and families. Credit card debt here has been inching up, but how big is the problem and how much of a risk does it pose? What should borrowers be taking note of when it comes to managing their credit card debt?

Video: https://www.youtube.com/watch?v=hZZwwqdfrSI

Credit card debt on the rise

Household debt levels in Singapore are largely under control, thanks in part to borrowing curbs imposed in recent years[1]. Still, a small but growing group of borrowers continue to struggle with mounting credit card debt.

Credit card debt made up about 4.3 per cent of all consumer loans in 2016 - roughly on par with 2015's 4.2 per cent, according to data from the Department of Statistics[2]. This capture ending credit card balances that remain unpaid at the end of the month.

The Monetary Authority of Singapore (MAS) introduced new rules to curb unsecured borrowing in 2013, as part of efforts to put a lid on rising household debt. Among other safeguards, an industry-wide borrowing limit was introduced in June 2015. Under this rule, financial institutions are not allowed to extend further unsecured credit - which includes credit cards - to borrowers whose debts exceed a prevailing limit. This limit is being phased in over four years - starting with 24 times a borrower's monthly income from June 2015, to 18 times from June 2017 and 12 times from June 2019.

These regulations helped lower total debt among Singapore households. Growth in outstanding credit card balances moderated from a peak of 14 per cent year-on-year in the second quarter of 2012, to an average of 2.6 per cent in the first nine months of 2017, data from Credit Bureau Singapore (CBS) showed[3].

But households are still holding on to significant credit card debt. Banks wrote off a total of S$128.3 million in bad credit card debt from January to May this year, according to MAS data. On a per card basis, bad credit card debts written off reached S$3.34 per card in May 2018 - a level last seen in 2005. This means borrowers were persistently unable to repay these loans, forcing banks to write them off.

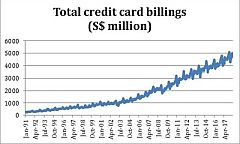

This comes as the number of credit cards in circulation here has risen rapidly over the past decade according to MAS data[4] - from about 6 million in May 2008 to a whopping 9 million as at May 2018, a 50 per cent surge.

The MAS noted in its November 2017 Financial Stability Review[5] that there are still "a number of borrowers who are increasing their level of indebtedness above 12 times their monthly income".

Why is credit card debt climbing? What are the risks?

Consumers accumulate credit card debt for a variety of reasons, including spending above their means, bouts of unemployment and paying for essentials. Credit cards are an increasingly popular mode of payment, which might be part of the reason why borrowing is on the rise. Financial institutions offer a wide array of perks to encourage consumers to spend more on their cards - from cashback and airline frequent flyer miles to free gifts and sign-up offers. In addition, it is now easier than ever to make payments with a credit card - the rise of e-wallet apps like Apple Pay, Android Pay and Samsung Pay, for example, allow users to tap and pay for goods and services at contactless payment terminals.

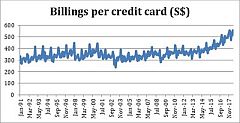

The numbers show that people in Singapore are increasingly reliant on their credit cards. Monthly billings per card hovered between S$300 to S$400 from the mid-1990s to early-2010s, but have started rising above $S400 in recent years[6]. In May 2018, monthly billings per card amounted to about S$555, after reaching S$514 in April and S$537 in March.

Even as consumers spend more on their credit cards, interest rates are also on the rise - making it tougher for some to meet their repayment obligations. After the global financial crisis, major central banks around the world used ultra-low - even negative - interest rates as a tool to revive economic growth. Lower interest rates make it cheaper and more appealing for households and businesses to borrow. Since then, however, the global economy has recovered and growth has picked up. As a result, policymakers have gradually started raising rates. The United States Federal Reserve has been leading the pack of developed market central banks in lifting interest rates from the ultra-low levels implemented in the wake of the global financial crisis.

Interest rates in Singapore are highly correlated with global rates - the Fed's latest rate hike announcement in June 2018 sent the three-month sibor, or Singapore inter-bank offered rate, used to price home loans - to its highest level since 2008. Credit card interest rates are also rising in tandem with these broader increases, making it more expensive to borrow.

Reducing the cost of credit card borrowing

1. Pay credit card bills on time and in full

Credit card users typically fall into two main categories - "transactors" and "revolvers". Transactors pay their credit card balances in full every month and avoid paying interest. Revolvers carry credit card debt from one month to the next, paying interest on their average daily balance.

Credit card borrowing is extremely high-stakes - interest rates are astronomical at over 26 per cent a year. Rollover balances also incur late-payment charges that are tagged on to the outstanding principal, further magnifying the amount owed. As a result, credit card debt can snowball very quickly - which means being a revolver can be very expensive. Clearly, the most effective way to avoid falling into credit card debt is to pay off balances promptly and in full.

2. De-clutter your wallet

There is no magic number for the number of credit cards a person should have - it depends on spending behaviour, financial goals and personal money management.

A consumer who pays off balances in full and on time every month can consider having multiple cards to take full advantage of benefits such as cashback, frequent flyer miles and discounts. However, holding more cards also means greater potential for racking up debt.

Besides limiting your borrowing, having fewer credit cards also means fewer bills to keep track of each month - which can help you stay on top of your credit card payments and avoid incurring late fees or interest.

3. Consider switching to a personal loan

Instead of dealing with sky-high interest rates, consumers can consider using personal loans to pay off credit card debt. Taking on more debt might sound counterintuitive, but personal loans can actually help borrowers save money.

Personal loans are "unsecured" loans, which means that unlike secured loans, they are not backed by collateral - like a house or a car - that lenders can repossess if borrowers default. This means personal loans have higher interest rates than secured loans, but they often offer lower interest rates than credit cards.

Personal loans can be used to consolidate your credit card debt into one manageable account, as long as you stay within your borrowing limit. This will help cut back on the number of bills to pay and keep track of every month. Instead, a personal loan allows borrowers to pay a fixed amount monthly.

There are three main types of personal loans available in Singapore. Personal instalment loans - the most common type - provide a lump sum of cash upfront, with monthly repayments. The second type is a credit line, which allows borrowers to draw money as needed and pay interest only on the amount borrowed. Finally, balance transfers allow borrowers to consolidate outstanding debt into one account, with fixed monthly repayment schedule.

One of the newest and most attractive options on the market is the Standard Chartered CashOne Personal Loan, which offers guaranteed flat interest rates as low as 3.88 per cent per annum (EIR: 7.63 per cent annum) regardless loan amount and tenure. This rate is exclusively available on personal finance comparison website SingSaver, for a limited period. Borrowers can borrow up to four times their monthly salary, capped at S$250,000.

Singaporeans have a total outstanding debt of about S$70.4 billion on credit cards and personal loans, according to 2017 data from the Department of Statistics Singapore. But if each borrower took time to consider their personal loan options, Singaporeans could collectively save more than S$500 million on interest payments every year (assuming S$23.5 billion in personal loan debt and an interest rate of 3.88 per cent per annum).

While personal loans can be less costly than credit card debt, however, they still come at a relatively high price. For some borrowers, personal loans might not be a viable long-term solution - especially if their debt is the result of overspending or lack of income. Before taking out another loan, these borrowers should consider identifying and tackling the root cause of their debt through financial re-evaluation or lifestyle changes. Ultimately, borrowers need to do their research and make sure personal loans are financially viable for them.

Media Contact: -

Mr Jeff Oon

Mobile: 97951580

Email: Jeffrey.oon@singsaver.com.sg

[1] MAS Financial Stability Review 2017: https://bit.ly/2M6YuMt

[2] Singapore in Figures 2017: https://bit.ly/2KyMsqv

[3] MAS Financial Stability Review 2017: https://bit.ly/2AJHHus

[4] MAS Monthly Statistical Bulletin, May 2018: https://bit.ly/2KDKl4Y

[5] Financial Stability Review 2017: https://bit.ly/2AJHHus

[6] MAS Monthly Statistical Bulletin, May 2018: https://bit.ly/2KDKl4Y

Topic: Press release summary

Source: SingSaver

http://www.acnnewswire.com

From the Asia Corporate News Network

Copyright © 2024 ACN Newswire. All rights reserved. A division of Asia Corporate News Network.

|

|

|

|

|

|

|

Latest Press Releases

Masverse Unveils Groundbreaking Blockchain Platform

Apr 27, 2024 02:40 HKT/SGT

|

|

|

Spritzer Scores Big with 'Meet the Red Legends' Event for Football Fans

Apr 26, 2024 23:00 HKT/SGT

|

|

|

Announcing Mad About Marketing - A New Member of the Digital Sukoon Private Limited Family

Apr 26, 2024 22:25 HKT/SGT

|

|

|

FinTech Funding Continues to Surge as Second Edition of Dubai FinTech Summit Commences

Apr 26, 2024 21:10 HKT/SGT

|

|

|

TIME Interconnect Technology Limited Announces Final Results For The Nine Months Ended 31 December 2023

Apr 26, 2024 18:26 HKT/SGT

|

|

|

UK advertising reports GBP36.6bn spend in 2023

Apr 26, 2024 17:30 HKT/SGT

|

|

|

CanSinoBIO CSO Shares the Latest Results of the Company's Globally Innovative Pneumococcal Vaccine

Apr 26, 2024 15:36 HKT/SGT

|

|

|

Edvantage Group Announces FY2024 Interim Results

Apr 26, 2024 13:43 HKT/SGT

|

|

|

Internationally Renowned Botulinum Toxin Experts Join WizMedi Bio's New Botulinum Toxin Development Project

Apr 26, 2024 13:27 HKT/SGT

|

|

|

Imexpharm Corporation Hosts Shareholders, Analysts and Potential Investors at its 2024 Annual General Meeting

Apr 26, 2024 13:16 HKT/SGT

|

|

|

|

|

More Press release >> |

|

|

|

|

|

|

|

|